China outlook – A bumpy path to reopening

- 01 December 2022 (7 min read)

Key points

- China’s economic outlook continues to hinge on the path of the pandemic and Beijing’s response

- We expect the authorities to pave the way for a reopening, but that path will be bumpy and uncertain

- Falling exports – partially offset by a less bad property market – call for continued policy accommodation

COVID-19 response fails to keep up with virus

Three years into the COVID-19 pandemic, while most countries have exited emergency responses, China remains wedded to a rigid containment strategy. 2022 was a particularly difficult year for the Chinese economy, with the impact of rolling lockdowns exacerbated by a collapsing housing market and stiffening external headwinds – manifested in rising food and energy prices, escalating geopolitical tensions, and tightening global financial conditions. Beijing has tried to mitigate these shocks by easing counter-cyclical policies and finetuning its COVID-19 response after the Shanghai debacle. But those moves have failed to prevent a steep decline of economic growth. With annual GDP gains expected to more than halve to about 3% from 8.1% in 2021, Beijing is set to miss its growth target for the second time in three years.

The outlook for the economy will continue to hinge on the evolution of the pandemic and Beijing’s response. Continuing with draconian controls against repeated COVID-19 flare-ups will likely prolong the economic stress, creating permanent scarring in the economy and society. The housing market remains a wild card, as it struggles to find a bottom against depleting home-buyers’ confidence and acute financial stress among property developers. Exports – once a strong engine of growth – have also started to sputter and will likely lose further steam as developed economies fall into recession. These challenges will complicate Beijing’s counter-cyclical policies and make next year’s outlook more uncertain than usual. Below, we explain in detail these four drivers of the economy and the risks to our assessment.

Changing tack to reprioritise the economy

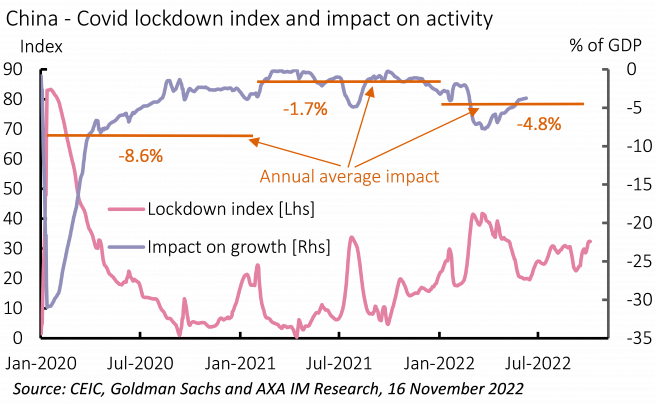

Starting with the pandemic, developments over the past year have likely brought two revelations to Beijing. First, the virus is unlikely to disappear any time soon, and could continue to mutate turning the pandemic to endemic, which may already be the case outside China. Second, and related, the medical response has to adapt for a long fight against a constantly changing enemy. The brutal lockdown in Shanghai, which brought China’s largest city to a standstill, was a painful lesson that achieving zero infections against a highly transmissible virus will inflict tremendous economic and social costs (Exhibit 11). Calls for an exit from the Zero COVID Policy (ZCP) have since grown as China becomes isolated from the rest of the world.

Beijing’s reluctance to change is likely a result of three considerations. Medically, China is not ready to exit the ZCP with a low immunity rate among its vast population and limited medical resources, which could prove insufficient to deal with increased severe cases upon reopening. Economically, the ZCP had been seen as a success not long ago for contributing to China’s growth outperformance and gains of export market share before this year. Finally, altering a policy, extolled as an emblem of China’s superior governing system ahead of a once-in-a-decade leadership reshuffle, was seen as unwise politically.

These arguments, however, have been weakened by recent events. The economic calculation has clearly shifted, reflected by the higher costs of tackling Omicron compared to the Alpha or Delta variants. Meanwhile, the conclusion of the 20th Party Congress has helped remove a major political uncertainty and refocus the party’s attention on its core objective of delivering growth and prosperity. The remaining hurdle is weak medical defences. Hence, moves to build such a defence should be seen as preparation for an exit from the ZCP.

Our baseline view for 2023 rests crucially on the assumption that the ZCP will be adjusted for an eventual reopening of the economy. We see this proceeding in three phases. Phase one focuses on getting the public medically and mentally ready for a change. This involves raising the vaccination rate (particularly for the elderly), introducing antiviral drugs, constructing more field hospitals, and reshaping public consensus to ease people’s fears of the virus. These changes are already underway and the latest announcement from Beijing of 20 measures to fine-tune the COVID-19 strategy suggests more is to come. Phase two puts the emphasis on reopening the domestic economy by easing social and mobility restrictions, reducing mass testing, and abandoning the frequent use of ‘static management’. A broad liberalisation within China is assumed to be reached by the middle of next year. The final step is to open the border with the rest of the world through successive reductions of quarantine restrictions for visitors.

It is important to reiterate our long-held view that no official announcement on ending the ZCP will be given until, perhaps, full liberalisation is achieved. But under the ZCP banner, we see the emphasis shifting from achieving zero infections at all costs to ‘dynamically adjusting’ the strategy to reprioritise economic normalisation. Investors therefore need to pay more attention to what Beijing does than what it says.

There is however considerable uncertainty around this baseline view. It is entirely possible that the fear of exposing China’s vast unvaccinated population to a virulent virus continues to hold Beijing back from reopening. And even if the ZCP is adjusted, the path could be bumpier than hoped. Too slow a change will do little to save the economy, while too fast an exit could lead to surging infections and hospitalisations that overwhelm the public health system. The ensuing social backlash could set back the reopening and economic recovery. We have built a cautious forecast – including a negative quarter of growth followed by only a partial recovery – to account for potential hiccups in this transition, but the actual path ahead could be bumpier still.

Property and exports switch sides

Besides the pandemic, the ongoing property market turmoil has also rattled the economy and financial markets. Fears of contagion to the household sector and banking system – following the mortgage boycott instance – prompted the authorities to ease property policies. But this was barely enough to slow the deterioration of conditions. The good news is that the policy wind has shifted further with Beijing now taking more substantial steps to ease developers’ funding stress. The bad news is that there are no easy fixes to the structural imbalances, with an overhang of housing supply in lower-tier cities and excess leverage at many private-sector developers. After abruptly pricking the bubble, Beijing now must manage its fallout. We expect further policy support to stabilise the market next year, helped by easing COVID-19 controls. But there will unlikely be a vigorous rebound of activities until structural challenges are tackled.

The external sector is set to become less supportive of the economy next year. After acting as a solid engine of growth since 2020, export activity has faltered lately and is expected to contract as developed economies slide into recession. In addition, rising geopolitical tensions between China and the US – notably in the area of advanced technology – could further impact an already soured trade relationship. The loss of this export growth contribution could add to the urgency for Beijing to ease COVID-19 controls to revive domestic demand.

Better transmission improves policy efficacy

The multitude of economic headwinds call for continued accommodation from China’s counter-cyclical policies. Compared to this year, policy efficacy may improve in 2023 if easing COVID-19 controls and stabilising property market can help to unclog policy transmission channels. On the monetary side, the room for aggressive easing is limited by concerns about currency depreciation and capital outflows, while tightening is unlikely given the uncertain path of the economy. Incremental policy exit is possible later in the year only if economic reopening proceeds smoothly. Fiscal policy will likely stay supportive too, but Beijing may struggle to repeat some ad-hoc, frontloaded, stimulus implemented this year given the already stretched fiscal balance sheets of local governments. With reduced potential for conventional stimulus, there are few options left to bolster growth other than freeing the economy from the grip of the pandemic.

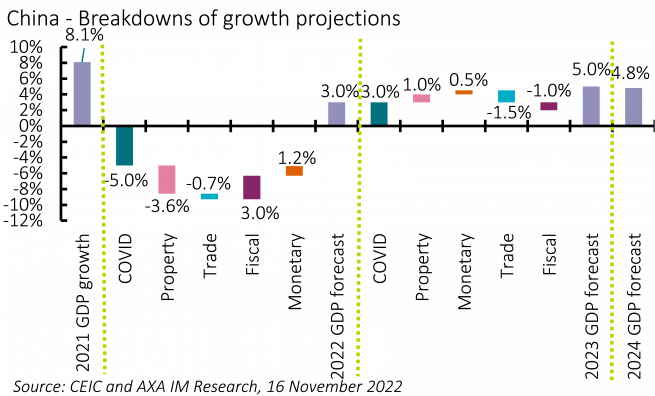

Exhibit 12 shows how our above-consensus 5% growth forecast for 2023 is derived. This is followed by a slight moderation to 4.8% in 2024 as the economy reverts to trend. The biggest swing factor in our forecast is the ZCP, which offers a two-sided risk. However, we consider the chances of inaction, or delayed action, from the authorities as greater than proactive action. In an adverse scenario of China continuing its current pandemic response for another year, we think the economy would suffer from deeper economic scarring and further reduced space for counter-cyclical policy. Annual growth could fall to 3.5% or lower in that scenario even with the help of a low base.

Our views for 2023

Read our full outlook to find out more about our experts' views.

Read our regional outlooks

US outlook – Mild recession to see inflation fall

Eurozone outlook – Difficult roads ahead

UK outlook – Navigating troubled waters

Japan outlook – Recovery appears set to continue

Emerging markets outlook – Darkest before dawn

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.