ECB Review: Unconvincingly dialling back

- 12 September 2024 (5 min read)

A second rate cut as expected.

In line with our long held call (unchanged since September 2023), the ECB Governing Council decided to cut the depo rate by 25bps to 3.5% at its September meeting. Consistent with the March GC decision on its operational framework to reduce the spread between the depo and the refi rate, the latter is now 3.65% (-60bps) with no expected meaningful ramifications as long as ample excess liquidity remains. In its press statement, the ECB reminded that the deposit facility rate is “the rate that steers the monetary policy stance”.

Further guidance is for later (maybe).

The ECB press statement kept the same sentence from previous meetings: “The Governing Council is not pre-committing to a particular rate path”. As we argued in our preview, the quarterly frequency of data on which the ECB relies to make its judgement is key. Q2 data have been reassuring enough for the ECB to continue to dial back the restrictiveness of its monetary policy, but not convincing enough to alter its forward guidance to more proactively guide about future cuts - possibly owing to the fact that the GC is broadly happy with market pricing 40bps worth of cuts by the end of the year. Furthermore, uncertainty runs high on upcoming budget sequence in a few member states, as well as the election outcome in the US. During the press conference, President Lagarde ventured to highlight the proximity of the October meeting which given their data-dependence, rather than data-point dependence makes very unlikely a cut at the October meeting in our view. We find ourselves surprised that still 13bps worth of cuts are still priced for that meeting. Otherwise, the market reaction has been relatively muted, not quite reflecting the hawkish tilt of the meeting.

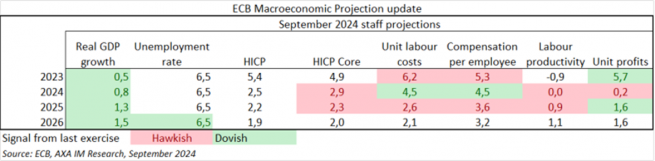

Hawkish tilt in forecast revisions.

Despite a significant miss in their Q2 GDP forecast (in magnitude: 0.2ppt and composition), we were surprised by the only slight downward revision (-0.1pp across the forecast horizon) in ECB’s forecasts, projecting euro area growth at 0.8%, 1.3% and 1.5% in 2024/25/26 respectively, remaining above our own (0.7%/0.9% for 2024/25). The dovish tilt that these could have sent was overshadowed by upside revisions in domestic prices pressures, across compensation per employee and labour productivity (Exhibit 1), fuelling 0.1ppt upside revisions in core inflation forecasts to 2.9% and 2.3% in 2024 and 2025. Said differently, in ECB’s view, weaker-than-expected domestic demand in Q2 24 is unlikely to repeat and thus does not carry any downside in consumer prices going forward. In fact, quarterly core inflation path has been revised up significantly for the three first quarters of 2025, leading to a 0.1ppt upside revisions in headline quarterly path but in Q4 25, still landing at 2.0% y/y.

Our call is unchanged for next cut in December.

We maintain our long-held call of a 25bp rate cut in December, and two more in March and June next year. While in principle live, we think it would take quite a shocker on the growth and inflation data-flow front for the ECB to cut rates again in October. Running into the December meeting (12 December) which will unveil the first batch of 2027 ECB’s forecasts, Q3 24 euro area negotiated wages will be published on 19 November and compensation per employee/profits on 6 December.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.