China – Eyes on trade fragmentation

- 19 September 2024 (5 min read)

KEY POINTS

Tariffs would threaten economy

The upcoming US election could significantly affect China’s economy, primarily through trade fragmentation. Both presidential candidates have discussed tariffs, though Donald Trump has threatened much larger increases than Kamala Harris – up to 60%. Exports have been a crucial driver of China’s economic growth, especially considering its several domestic challenges. The possible increase in US tariffs on Chinese goods could exert considerable pressure on China, subsequently dampening overall economic growth. Moreover, further disruptions in US-China trade relations could erode investor confidence. In recent years, China has become less attractive to foreign investors due to increased government intervention. Additional tariff hikes would heighten uncertainties, threatening to further reduce foreign investment in China.

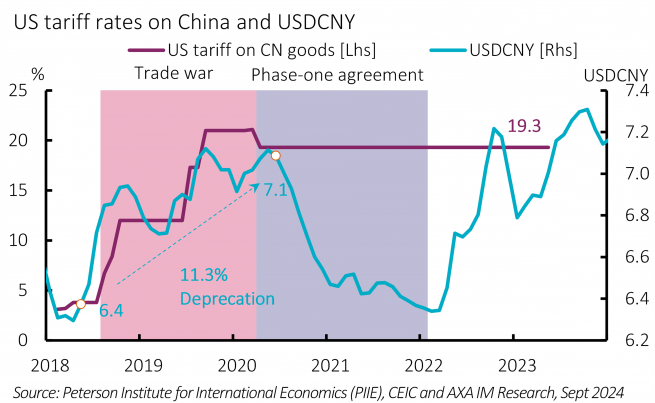

In Trump’s first term average US tariffs on Chinese goods surged from around 4% in early 2015 to 21% by late 2019, settling at 19.3% following the Phase-One agreement in early 2020. As a result, Chinese exports to the US dropped sharply in 2019, partially recovering in 2020. On average, exports to the US declined by 3% annually between 2018 and 2020, partially mitigated by the yuan’s depreciation. The yuan fell by 11.3%, from 6.3 to 7.1 against the US dollar (Exhibit 5), as the People’s Bank of China allowed devaluation in line with market forces.

If a blanket tariff of 60% on Chinese goods were imposed, based on 2023 export values, Chinese exporters would face over $200bn additional tariffs annually, equating to 1.2% of China’s GDP. As in the previous trade dispute, such a tariff increase would likely lead to a natural appreciation of the US dollar (depreciation of the yuan), which could mitigate some pressures. Nevertheless, the impact could still be significant and poses two major challenges.

A persistent negative output gap in China’s economy has led to a low-inflation environment, increasing the risk of entering a debt-deflation loop. A decline in external demand due to higher tariffs would slow growth, exacerbate this output gap and reinforce disinflationary pressures, including an increase in unemployment, particularly in export-dependent sectors, further weakening the labour market and dampening consumer confidence further.

Higher US tariffs could also trigger capital flight from China. The yuan is already weak due to a strong US dollar and China’s economic slowdown. Further tariff hikes could push the currency to new lows with significant yuan depreciation possibly triggering capital flight, particularly if combined with slower economic growth, stock market declines and worsening risk perceptions. Both domestic and international investors may seek more stable/profitable opportunities elsewhere, particularly if they anticipate prolonged economic challenges. The scale and immediacy of capital flight would also depend on the severity of any tariff increases, the broader economic environment, and the Chinese government’s response to these pressures, but could further destabilise China’s economy.

Despite these challenges, the impact of tariff increases could be less pronounced than in 2018. China has increasingly diversified its exports away from the US and strategically enhanced a deeper integration into key global supply chains – such as semiconductors, batteries and solar panels – which may offer some protection against future trade disruptions. However, these new supply connections could be more vulnerable to sanctions, with third parties encouraged to observe – which US Democrats have made more use of – than pure tariffs, which Trump favours.

The US election therefore poses a risk to the fragile outlook for China’s economy whatever the outcome. However, the suggested scale of tariff increases proposed by Trump pose the biggest risks. Proactive and adaptive policy responses will likely be crucial in navigating these uncertainties as well as delicacy in handling other geopolitical developments.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.