UK reaction: Looser labour market conditions point to further cut

- 15 October 2024 (3 min read)

The latest labour market data point to an additional cut at the Bank of England’s meeting in November. The Labour Force Survey data showed a chunky 373K increase in employment in the three months to August and the unemployment rate edged down again to 4.0%, lower than in the previous three months and the level this time last year. Ongoing sampling issues, however, mean the data are unreliable and should be taken with a large pinch of salt. Note the survey reached an average of 88.5K individuals with a response rate to 42.8% (around 38k respondents), whereas in H1 2024, those figures were 53.1K and 17.6% (around 9k respondents), respectively.

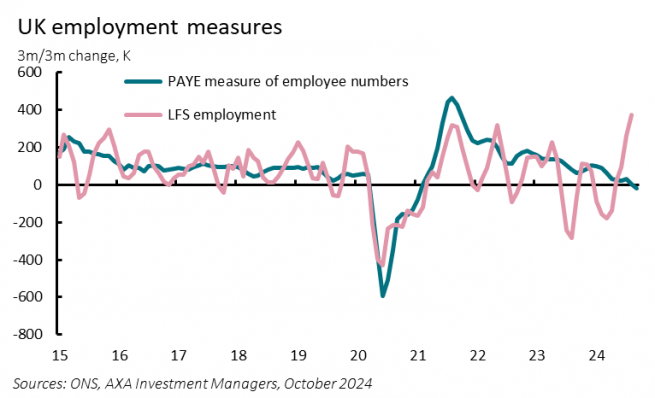

Other measures continue to point to looser conditions. The number of vacancies, for instance, fell for the 27th consecutive period in the three months to September. And the PAYE measure of employee numbers was broadly unchanged in September – it fell by 15K on the month – after a drop of 35K in August, the largest since the early stages of the pandemic. The ONS also noted that year-over-year growth in both the Workforce Jobs – a measure based on business surveys – and the PAYE measures has slowed significantly over the past 18 months or so. The KPMG/REC Report on Jobs survey, meanwhile, suggested that some firms were putting hiring decisions on pause until after the Budget on October 30th, due to concerns over potential tax changes.

Likely most important for the BoE, though, will be the ongoing deceleration in wage growth. Average weekly earnings ex. bonuses fell to 4.9% - its slowest pace since June 2022 – from 5.1% in the three months to July, driven by declines in both public and private sector pay regular pay; the former slowed to 5.2%, from 5.7%, and the latter to 4.8%, from 5%. Total earnings – which include bonuses – fell further to 3.8% - over a three-and-a-half-year low - from 4.1%, though the disparity largely reflected base effects, given NHS workers and civil service workers were given one-off bonus payments across the summer in 2023. On a 3-m annualised basis, total earnings grew by 2.7% and ex-bonus payments by 4.4%.

On balance, the latest labour market data should convince a majority of MPC members in November that enough slack is developing to support a gradual deceleration in wage growth back to more sustainable levels over the next year or so. Note the BoE’s Decision Maker Panel survey showing businesses expect wage growth to be around 4% in 12 months’ time. In addition, we expect a renewed decline in CPI inflation in September – released tomorrow morning – to 1.8%, with services CPI inflation slowing to 5.1%. Both point to one further cut in Bank Rate in November. Further ahead, the key risk remains the Budget; if the Chancellor tightens fiscal policy materially in order to close the so-called fiscal “black hole” then the BoE may be forced to tighten more aggressively to offset the hit to growth.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.