CIO Views: Bond returns potentially higher in 2025

- 06 February 2025 (5 min read)

KEY POINTS

Chris Iggo, CIO AXA IM Core

Steady income should not be overlooked

Many investors have been enjoying higher income returns as the average market-weighted coupon on bond indices has been rising since 2021 – and are likely to continue to do so as lower coupon bonds issued before 2021 mature. Over the last 10 years, the compound income return from a typical US dollar investment-grade index has been around 4%, and in Europe, the equivalent has been just over 2%. For US dollar high yield, it has been close to 6.5%. Given the rise in average coupons, income returns should potentially be higher going forward.

Of course, bond prices can be volatile. Unless bonds are held to maturity, losses can be incurred from shifts in interest rate expectations or credit spreads. To manage this risk, investors may choose strategies that have inherently less price volatility – like short-duration credit strategies. Or they can employ active managers who seek to maximise income and minimise price volatility, through hedging and other active decisions. Investors can also aim for income above the average index level through an allocation to higher-coupon bonds. Income returns are unlikely to match pre-2008 levels but are becoming more attractive given the broad increase in bond yields since 2021. With uncertainty surrounding the macro outlook, steady income returns should not be overlooked when building balanced portfolios.

Alessandro Tentori, CIO Europe

European government bonds: Liquidity-driven valuations

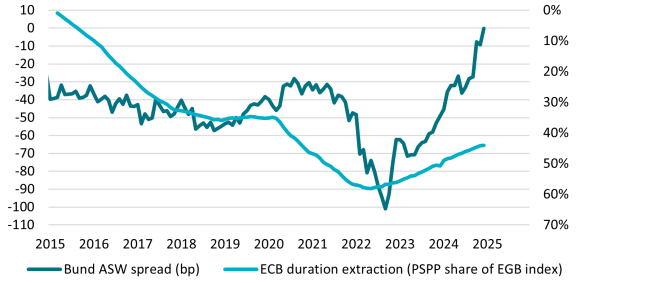

Fixed income investors might have noticed the rather large swing in the valuation of German government bonds (Bunds) relative to interest rate swaps in the post-COVID-19 period. In the two years to September 2022, Bunds became expensive relative to the interest rate swap curve. Since then, there has been a 100-basis-point (bp) cheapening of Bunds versus swaps. This has erased the ‘natural margin’ that risk-free bonds should have relative to risk-bearing bonds.

Looking at the Bund swap spread from a microeconomic perspective opens the door to variables like excess demand and collateral scarcity. These variables are linked with the activity of the largest bond player during the past decade: the European Central Bank (ECB). The chart below shows the relationship between the ECB’s footprint on the European government bond market and the Bund asset swap spread. The post-pandemic quantitative easing impacted the perceived scarcity of Bunds, thus raising liquidity concerns for Europe’s benchmark bond and pushing relative valuations to extreme levels. Similarly, the ECB’s decision to dial back its unconventional monetary policy operations from July 2022 put a lid on the liquidity spectre and reversed the course of Bund spreads. Indeed, other European government bonds have cheapened against

swaps as a result of the reduction in ECB buying and concerns about increased supply. For some investors, this will have made European government bonds a more attractive fixed income asset relative to both swaps and corporate bonds.

Ecaterina Bigos, CIO Asia ex-Japan

Region in waiting

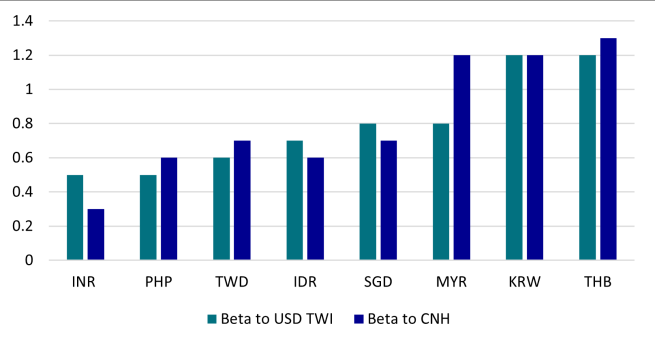

Asia’s macroeconomic environment has become increasingly challenging from a growth, monetary policy, and currency perspective. Trade tariffs, the Federal Reserve’s (Fed) interest rates path and US dollar strength make up the overarching headwinds. The US policy agenda on tariffs is the biggest direct vulnerability given many Asian countries run some of the largest bilateral trade surpluses with the US, but also indirectly, due to relatively high economic interdependency with China. While inflation eased in most Asian economies in 2024, the average remains above most central bank targets, hence the region's low real rate relative to a stronger US dollar and higher core rates add to its challenges. Fed policy path remains critical as it could intensify capital outflows from countries that ease rates too aggressively. Even in an environment of more measured tariff hikes, investor flows are likely to maintain a dollar bias. Most Asian currencies have depreciated against the greenback, particularly in the fourth quarter of last year, driven by the potential for fewer Fed interest rate cuts. Currencies will likely be the pressure valve for adjusting to any growth shock from tariffs, with intra-

regional correlations likely higher initially, before policy choices, domestic imbalances and relative fiscal space in the various economies drive divergence.

*Source: Deutsche Bank, Bloomberg Finance LP, Jan 2025. Betas calculated over last two years, except for INR where betas are calculated during the peak of trade wars during President Donald Trump’s first term (and before the low FX policy volatility regime since late 2018)

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

CIO team opinions draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Rates | Budgetary concerns and US politics suggest higher volatility even if rates in fair-value range | |

|---|---|---|

US Treasuries | 10-year yield likely to stay below 5% unless view on direction of Fed policy changes | |

Euro – Core Govt. | German Bund yields reflect weak growth outlook and lower ECB rates | |

Euro – Peripherals | Spain continues to be preferred; French government bonds subject to ongoing political risk | |

UK Gilts | Bank of England expected to cut rates in February; market anticipating fiscal update in March | |

JGBs | Bank of Japan’s January rate hike reflects inflation concerns; negative on JGBs | |

Inflation | While real yields are attractive, the break-even rate does not fully reflect inflation risks |

Credit | With growth resilient, investor confidence in credit remains strong | |

|---|---|---|

USD Investment Grade | Credit yields are attractive; elevated valuations create vulnerabilities if rates keep rising | |

Euro Investment Grade | Modest growth, alongside lower interest rates support credit’s income appeal | |

GBP Investment Grade | Returns supported by cooling inflation and deeper rate cuts than what is priced in | |

USD High Yield | Stronger growth, resilient fundamentals, and higher quality universe are supportive | |

Euro High Yield | Resilient fundamentals, technical factors and ECB cuts support total returns | |

EM Hard Currency | Attractive income from higher quality universe than recent history |

Equities | Growth backdrop supportive but risks of tariffs hitting global trade | |

|---|---|---|

US | Earnings growth supportive; performance more balanced as AI bubble somewhat deflates | |

Europe | Valuations are attractive; low return expectations could be exceeded by positive surprises | |

UK | Markets need to see how government can improve growth prospects; lower rates will help | |

Japan | Solid combination of valuations and expected earnings growth | |

China | Signs of improving confidence but foreign investors need to see more policy support | |

Investment Themes* | Competition in AI to create more opportunities for beneficiaries of technology |

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.