Why it’s time to reconsider small caps

- 20 March 2025 (5 min read)

KEY POINTS

In AXA IM’s view, the combination of falling interest rates and cheap valuations for global small caps may currently offer an attractive opportunity for investors. We think it is time to consider revisiting your allocation to attractively valued small caps equities, potentially improving portfolio diversification by moving away from large caps. Furthermore, a quantitative investment approach such as that employed by AXA IM’s Equity QI team is particularly well-placed to deliver positive outcomes for investors within this space.

Attractive valuations

Small cap companies have historically traded at a premium to or in-line with large cap companies, this is no longer the case. Equity market performance has been dominated by mega-cap companies in recent years, notably large technology companies known as the ‘Magnificent Seven’, many of which benefit from the AI theme. One benefit of the lack of attention paid to small cap companies is that they now offer compelling return potential as they are trading on attractive valuations, particularly compared to their large cap peers.

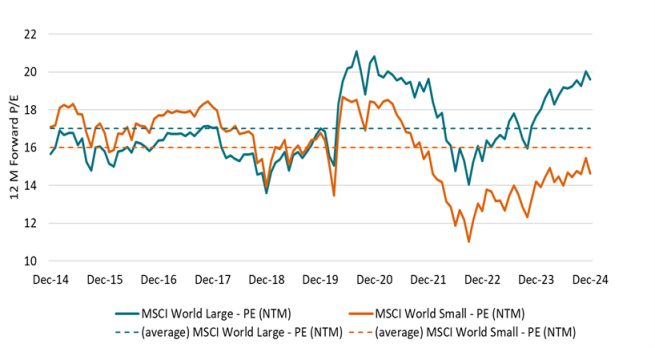

The chart shows that forward P/E (Price-to-Earnings) valuations are lower for the Global Small Cap universe than for the standard Global Large Cap universe. The valuation spread has diverged from 2020 and has widened. Not only are Global Small Caps attractively valued versus Global Large Caps, but also relative to their own history, given they are currently trading at a discount to their long-term average valuation. Conversely, Global Large Caps are trading at a premium to their long-term average valuation. Even when adjusting for earnings growth, small cap companies are cheaper than their large cap counterparts, and relative to their long-term average valuations, as measured by the Price/Earnings-to-Growth (PEG) ratio.

Large opportunity set with high dispersion of potential returns

While the small cap investment universe is attractively valued, it is also a deep universe of companies. Given this size, it is also unsurprising that there are plenty of attractive investment possibilities within the universe. In terms of earnings generation, it is also important to recognise that there is a larger gap between ‘good’ and ‘bad’ companies in the small-cap universe than in the large-cap one. Such a gap creates an increase in excess return generating opportunities (or alpha) for a savvy equity investor.

Given the risk of potential losses from allocating to poor quality companies, a diversified investment approach with the ability and skill to assess large parts of the investment universe consistently may be more likely to deliver consistent investment returns through time.

Bringing a quantitative approach to small cap equities

The breadth and depth of the market creates opportunities for skilled stock pickers who can analyse a large number of companies in a manner capable of identifying good investment opportunities while avoiding loss-makers, favouring an actively managed approach to investing in small caps.

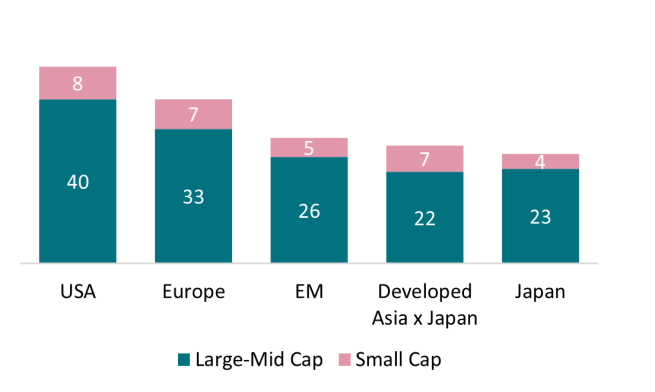

However, given the scale of the investment universe it would take a tremendous number of stock pickers to adequately research and monitor all global small cap companies on a continuous basis. The small cap universe suffers from traditional information scarcity, there is little coverage by traditional sell-side analysts, as shown in the chart below:

| Small cap | Typical benchmark | EQI investment universe |

| North America | 2,000 | 2,600 |

| Europe | 1,000 | 1,800 |

| Japan | 850 | 1,500 |

| Dev. Asia ex-Japan | 350 | 600 |

| Developed Market | 4,200 | 6,500 |

| Emerging Market | 2,000 | 4,000 |

| All Country | 6,200 | 10,500 |

Source: AXA IM, average sell-side analyst coverage of benchmark stocks as of January 2025, stock universe as of October 2024.

This is why a systematic investment approach like that employed by AXA IM’s Equity QI team is particularly powerful. Our team uses rich data sets (financial and non-financial information) and sophisticated analytics, including machine learning techniques, to assess 10,500 small cap companies across the world using a consistent investment framework.

The Equity QI team develops detailed views on the business quality, earnings profile, and valuation of every investable company within the global small cap equity universe on an on-going basis, identifying inefficiencies and opportunities in this vast, under-researched small cap universe.

Investing in Small Caps with a multi-factor approach

In conclusion, there are at least three reasons to reconsider an allocation to global small caps:

- Attractive valuations compared to large caps, and relative to history;

- Large return dispersion means more opportunities for a skilled active manager to exploit;

- A large and increasingly under-researched universe of companies.

Given the sensitivity of small caps to macroeconomic changes, active management remains crucial. At AXA IM, we take a multi-factor investment approach (focused on value, momentum and quality factors) to build a diverse portfolio that benefits from advanced machine learning and modelling techniques for a detailed analysis of companies, while incorporating ESG information in portfolio construction.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.