Inflation-linked bonds: more than just inflation

- 08 August 2024 (3 min read)

With inflation expected to be more uncertain and volatile than in the previous decade, investors may want to consider hedging the inflation risk of their portfolios. Inflation continues to edge towards central bank targets, however with stickiness in services’ sector inflation and some base effects, there could be some bumps along the way to the desired 2% level. This suggests investing in inflation-linked bonds may be an option to mitigate against this sticky inflationary environment.

At the beginning of 2024, we explored why investors may still want to consider inflation linked bonds in a falling inflationary environment1 . Many of the reasons mentioned then still apply now. In particular, the fact that inflation risk remains tilted to the upside. This continues to be a focus with the upcoming elections creating uncertainty over whether governments will be able to reduce public deficits or if it could lead to increased borrowing. Along with political uncertainty, geopolitical tensions and climate change concerns are other aspects that may slow the disinflationary march. We think it is therefore still relevant to consider inflation-linked bonds within a portfolio.

- PGEgaHJlZj0iaHR0cHM6Ly9jb3JlLmF4YS1pbS5jb20vcmVzZWFyY2gtYW5kLWluc2lnaHRzL2ludmVzdG1lbnQtc3RyYXRlZ3ktdXBkYXRlcy9mdW5kLW1hbmFnZXItdmlld3MvZml4ZWQtaW5jb21lL3doeS1jb25zaWRlci1pbmZsYXRpb24tbGlua2VkLWJvbmRzLXlvdXItYXNzZXQtYWxsb2NhdGlvbiI+V2h5IGNvbnNpZGVyIEluZmxhdGlvbi1saW5rZWQgYm9uZHMgaW4geW91ciBhc3NldCBhbGxvY2F0aW9uIHwgQVhBIElNIENvcmUgKGF4YS1pbS5jb20pPC9hPg==

Why Inflation Linked Bonds remain relevant

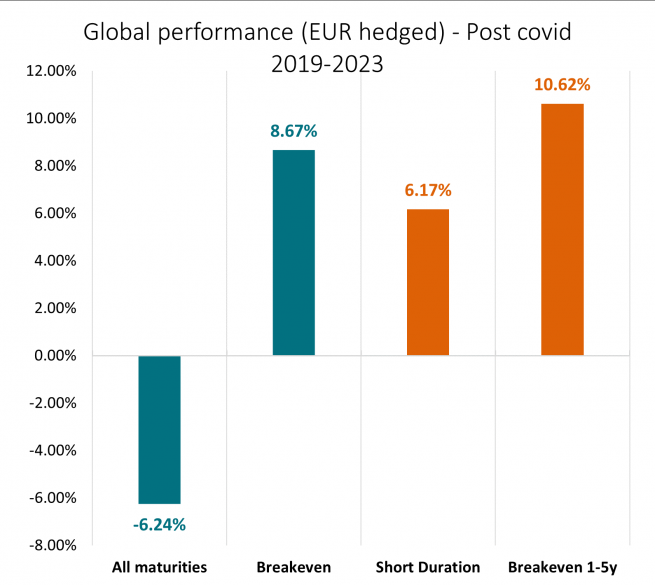

In rising inflationary environments, it is quite natural to consider inflation-linked bonds and to appreciate what they can offer to a portfolio. As inflation-linked bonds total return is a function of inflation indexation and the change in real interest rates, when inflation expectations rise, inflation-linked bonds tend to outperform their nominal counterparts which has been the case in the post-COVID period.

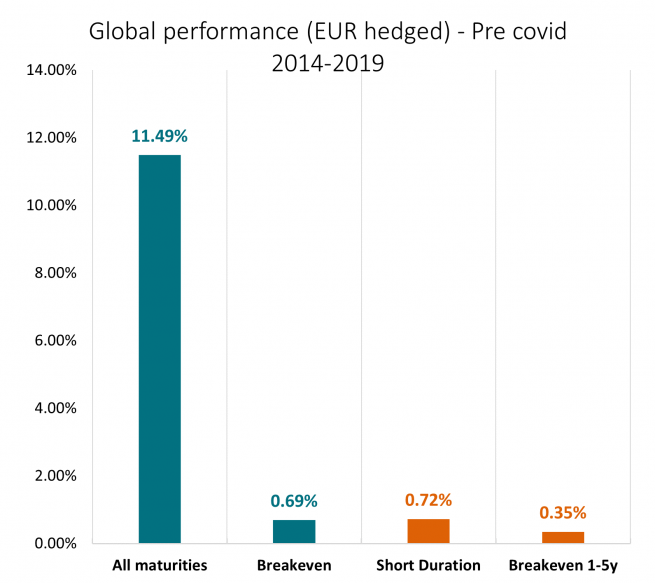

However, even in a low inflation environment, inflation-linked bonds may improve the risk adjusted returns of a portfolio as they tend to not correlate with stocks or other fixed income assets. Therefore, in stable & low inflation environments, we would expect inflation-linked bonds to deliver a performance close to their nominal counterparts. This has been seen historically in low inflation environments such as before COVID.

Total and relative (breakeven) performance of inflation linked bonds universe

All maturities ~9y of duration and short duration ~3y.

Breakeven performance signals the outperformance (or underperformance) of inflation-linked bonds relative to a comparable nominal bonds’ universe.

How to make the most of ILBs

At the moment, with real interest rates still in restrictive territory and growth expected to be subdued, long duration positions remain attractive. However, as central banks begin to cut interest rates, the front end and the steepeners positions should begin to look more attractive. This need to adjust duration allocation in order to optimise returns, is seen in the charts above, reflecting how each segment of the curve (front end and long end) have performed in different inflationary environments. We believe this demonstrates that taking an active approach to an investor’s inflation portfolio may be help to achieve better risk-adjusted returns.

The history from the past decade offers evidence that diversification within an inflation-linked bond portfolio may help investments from either credit-related events like the Euro Area crisis in 2011 and 2012 or duration swings such as 2022/2023. Not only should an inflation-linked bond global approach offer a better risk/return profile thanks to its diversification benefits, but we believe that there are broader opportunities available within a global approach than that of a local focus.

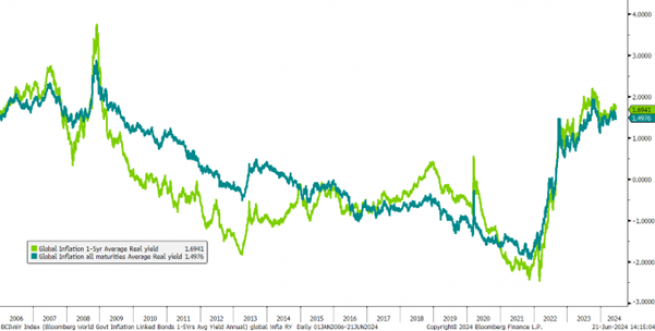

A global approach will tend to favour relatively higher real interest rates and, as a consequence, may maximize investors’ income adjusted for inflation. As the chart below shows, real rates remain in positive territory. We do not, therefore, expect them to subtract income to the asset class, unlike the past 10 years.

Likewise, a flexible active strategy may also bring value to the table by leveraging on seasonal inflation swings. A flexible approach should be able to allocate assets where inflation accruals are the sharpest and potentially benefit from seasonal patterns or structurally higher inflation.

Although we face a disinflationary environment, inflation risks remain tilted to the upside, so in the medium term, inflation-linked bonds may still have a role in mitigating against this risk. They can also play a broader role in a portfolio, offering investors diversification and low correlation to other investments without necessarily taking on additional credit risk.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.