China reaction: monetary easing delivered, now waiting for fiscal coordination

- 24 September 2024 (5 min read)

The PBoC unveiled a series of monetary policy measures following today’s unusual press conference, aimed at supporting the economy as the growth target becomes increasingly elusive. The newly announced package is designed to ease monetary conditions across the broader economy, with a particular focus on the housing market. The measures include reductions in the RRR, policy rate, outstanding mortgage rate, and minimum down payment ratio for second homes. Additionally, the re-lending programme for the housing stock buy-back scheme will be strengthened, and restrictions on the equity market will be loosened. This announcement aligns broadly with expectations, though it leans slightly stronger than anticipated. However, it is unlikely to outweigh the current entrenched economic downturn – coordination from fiscal policy is needed to ensure a good efficacy.

Rate cuts across the board and a special focus on properties

A 50bps reduction in the RRR, which applies to mid-sized and large banks, was announced, in line with expectations. This will bring the weighted average RRR down from 7.0% to 6.6%. The PBoC also promised an additional unexpected RRR cut of 20-50bps by the end of the year. The 50bps reduction will release 1 trillion Chinese Yuan (RMB) in long-term liquidity into the banking system, and further cuts in the coming months will continue to provide liquidity support to banks.

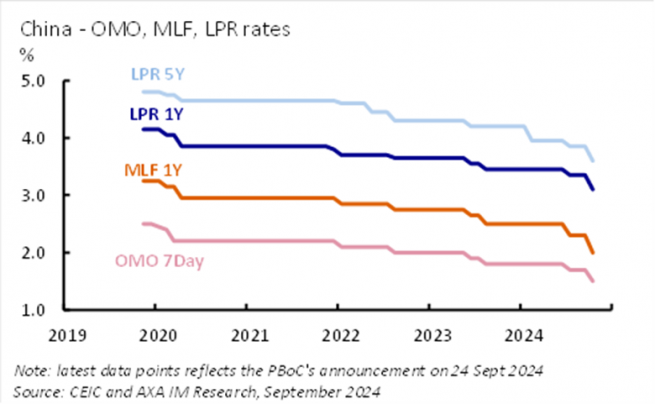

The 7-day reverse repo rate will be trimmed by 20bps, to 1.5% from 1.7%, as confirmed by Governor Pan Gongsheng, slightly exceeding expectations. This will result in a 30bps cut to the 1-year medium-term lending facility (MLF) rate to 2.0%, with deposit and Loan Prime Rates (LPR) also expected to drop by 20-25bps. According to Pan, these changes are "neutral" to commercial banks’ net interest margins.

The package includes further support for the property market. Existing mortgage rates will be cut by around 50bps on average, which is slightly more than expected. In addition, the downpayment requirement for second homes will be lowered by 10ppts to 15%. The PBoC has also enhanced the re-lending programme for the housing stock buy-back scheme, increasing the funding support ratio from 60% to 100%. The scheme's quota and rate remain unchanged at RMB 300 billion and 1.75%, respectively. The re-lending programme has been underutilised to date —only 4% of the quota was issued by the end of Q2—the enhanced funding ratio should improve policy execution and help reduce housing inventory.

Monetary easing alone unlikely to revive credit demand

While liquidity injections may help lower borrowing costs, they may not automatically generate credit demand. What is lacking in China’s financial system at the moment is not liquidity but genuine demand for credit. The reduction in mortgage rates in that sense is more welcome by households, but in itself is likely to be too small to restore consumer confidence fully. A persistent interest rate gap between new and existing mortgages, estimated at around 84 bps and this has now been reduced. Today’s rate cuts could save households RMB 150 billion in interest payments—equivalent to 0.3% of annual retail sales—and this boost to incomes may translate to higher spending. However, without a significant improvement in confidence, the saved mortgages from the rate reduction could be translated to increased household savings or another round of prepayments, amid the negative asset price outlook and homeowners concerns about their debt persist.

New instruments to support equity market

The PBoC also announced new measures to support the equity market. Qualified securities firms, funds, and insurance companies will be permitted to use funding from the PBoC to buy stocks through a swap facility. The quota for the first batch is set at RMB 500 billion, with the possibility of increasing it by up to two additional batches, contingent on its effectiveness.

In addition, a specialised re-lending facility for stock buybacks by listed companies and major shareholders will be established, with an initial quota of RMB 300 billion. Notably, this facility will be available to companies across different ownership types, including privately owned enterprises.

Good move, but can be better

While monetary easing is necessary, the scale of measures announced today is unlikely to be sufficient to reverse the current economic weakness given the severe lack of risk appetite and credit demand. The de facto fiscal austerity – with local government actions not reflecting central government ambition - remains the primary drag on growth momentum. A pragmatic rebalancing of responsibilities between central and local governments is essential to ensure smooth policy transmission and break this “austerity trap”.

Following today’s announcement, we maintain our growth forecast for 2024 at 4.8%, with slightly reduced but still present downside risks. A strong, coordinated fiscal policy in the near term is both important and necessary to ensure the effective transmission of today’s monetary easing measures. For 2025, we expect a GDP growth rate of 4.4%.

Related articles

View all articles

ECB update: Cautiously surfing the dovish wave

- by ,

- 07 October 2024 (3 min read)

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.