ECB update: Cautiously surfing the dovish wave

- 07 October 2024 (3 min read)

Little doubts of a 25bps rate cut in October

The September flash inflation print highlighted significant downside to ECB’s forecasts unveiled just a few weeks before. Crucially, core inflation came at 2.7% y/y in Q3 24 while ECB’s forecasts revised in September had 2.9% y/y. Given the surprise came from core components, the downside is likely to transpire at least through a few quarters. In our reaction to the print, we thought it was enough for the ECB to decide on 25bps rate cut in October (no rate cut expected previously at that meeting), also since President Lagarde expressed increased confidence in the timely return of inflation to target in her statement at the European Parliament. Such comments were also echoed by historically hawkish ECB board member Isabel Schnabel, while she also highlighted growth headwinds and softening labour demand, making clear the lack of willingness to fight market pricing which had over 90% probability a 25bps rate cut at the next meeting.

Weak domestic demand with little hope of (imminent) significant pick-up

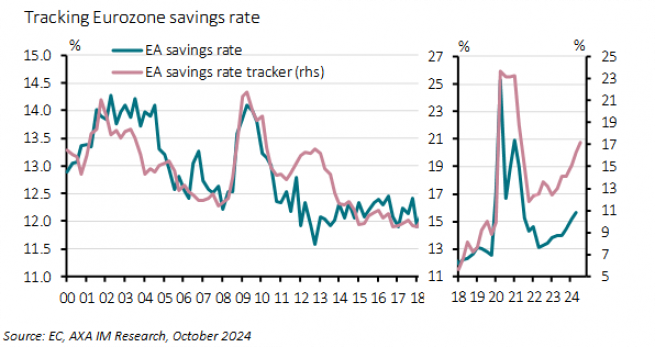

Euro area final domestic demand (aggregated private and public consumption and overall investment) contracted in Q1 and Q2 this year. While this was mainly led by investment, private consumption growth was anaemic, growing by an average 0.1% q/q in H1 24 – and contracting in Q2, despite significant real purchasing power gains. Latest business and consumer confidence surveys are consistent with our view of no imminent material domestic demand pick-up by contrast with ECB’s latest forecasts. We think that softening labour market, significant political uncertainty in Germany and France, and decent real deposit rates are likely to maintain household’s savings rate high, as suggested by our tracker (Exhibit 1), and delay the investment recovery. Downward revisions in these two countries in our latest global macro monthlywere the main driver for lower, still below consensus, euro area 2025 GDP growth forecast at 0.9% (consensus & ECB: 1.3%).

Our latest inflation forecast update shows ECB’s inflation target undershooting for most of 2025

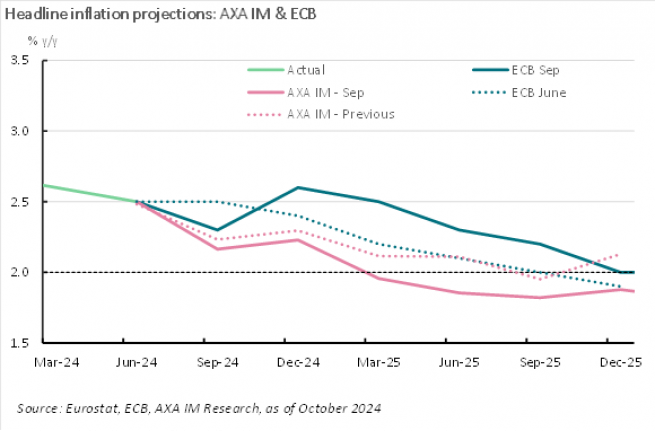

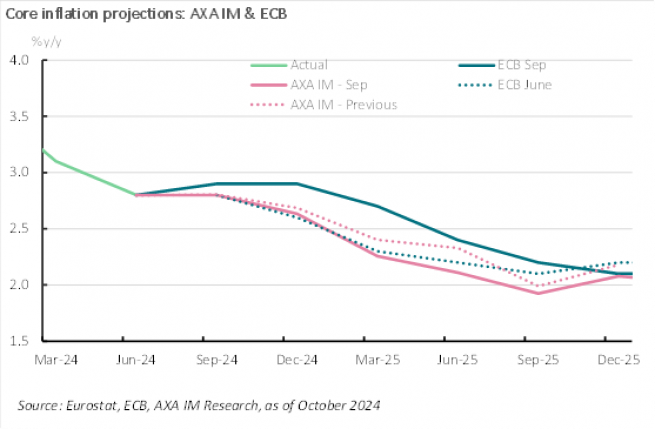

Beyond the abovementioned September inflation print, ECB’s 2025 inflation forecasts look too high. Exhibit 2&3 show similar difference between ours and ECB’s projections for headline and core inflation, implying that oil price assumptions play a likely minor role. Reflecting uninspiring domestic demand prospects, marked by the services-led consumption rotation running out of fuel - we have abated services (and goods) price seasonality. We now forecast headline inflation to come below ECB’s 2% target in the first three quarters of 2025, reaching a low in Q3 25 (1.8% y/y), while core inflation would continue its downtrend without too many humps and bumps.

We now expect back-to-back 25bps depo rate cuts through H1 25 to 2%, with a skew to the downside

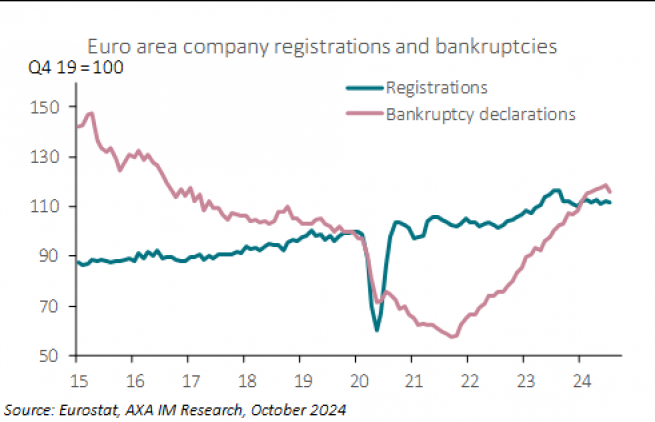

With already minimal deviation of actual inflation to ECB’s target, we think disappointing activity momentum will eventually lead the ECB towards a more forward-leaning policy bias, putting less – though unlikely to fully disappear - weight on its triptic (wage, productivity, unit labour cost) and justifying a step-up in ECB easing its restrictive stance from its quarterly forecast meetings – our expectation since September 2023. While our revised nominal policy rate would be within the vicinity of neutral by-end H1 25, it would be significantly more restrictive than in the previous fifteen years. As such, we cannot rule out the ECB going with a more aggressive easing cycle, either going 50bps in December or continuing for longer its easing cycle depending on data, but also on other central banks’ behaviour. Although euro area inflation sensitivity to euro currency tends to be small, the ECB will have to be mindful of its relative monetary policy stance, cautiously surfing the current overwhelming monetary policy easing narrative across all major advanced economies. Finally, Covid-19 and the 2022 inflation shock and their associated policy response have likely extended a growth cycle that started in mid-2013 that has yet to rollover. Although not an imminent concern, there is a significant net destruction of companies (Exhibit 4) in the euro area while fiscal leeway is very limited to non-existent across member states.

Related articles

View all articles

UK reaction: Still at target, but services remains sticky.

- by

- 17 July 2024 (3 min read)

China reaction: Q2 GDP marks the start of The Third Plenum

- by

- 15 July 2024 (5 min read)

US reaction: Services inflation makes pivotal shift lower

- by

- 11 July 2024 (5 min read)

US reaction: Labour market achieving balance

- by

- 05 July 2024 (7 min read)

European Parliament and French elections: Investor update

- by , Chris Iggo,

- 24 June 2024 (10 min read)

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.