US reaction: Inflation slowing in line, but nothing weaker

KEY POINTS

Headline inflation in July slowed to 2.9% - the first time it has been below 3% since March 2021. This was modestly below expectations, although with the monthly rise coming in at 0.155% vs the 0.2% consensus expected, the miss was modest (2.92%). Perhaps more importantly, core inflation also came in at 0.165% (versus a 0.2% consensus) and the annual rate slowed to 3.2%, in line with expectation, the lowest since April 2021.

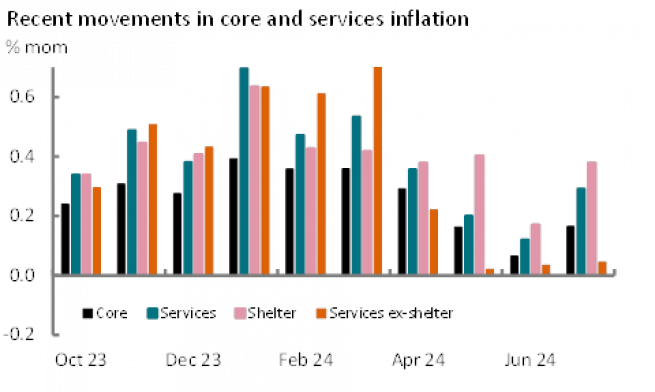

A breakdown of July’s inflation revealed several moving parts. Fuel prices continue to contribute to a lower headline rate. Annual motor fuel price inflation is -2.3%. Goods price disinflation persisted, with a monthly fall of 0.3% in July – the biggest fall since January – and the annual rate remaining at -0.4%. This was driven by further steep declines in used car prices – down 2.3% on the month – and a fall in clothing prices. Both of these developments are consistent with an ongoing softening in consumer spending, although household furnishing completed their second month of solid gains following sharp contractions in April and May. The Fed’s focus will continue to fall on services inflation, which remains elevated at 4.9% - albeit a joint 2½ year low. Overall these rose by 0.3% on the month, firmer than the previous two months’ readings, but still below the average pace of H2 2023 and far below the pace set in Q1 this year. Exhibit 1 below illustrates that this was dominated by firmer readings again in shelter. Shelter inflation rose by 0.38% on the month, with a small rise in owner equivalent rents (0.36% and still below every reading before last month), but rents on primary residences rose by 0.49%, the biggest increase in a year and a move that suggests a basic catch-up from last month’s weak reading, with rents now averaging around 0.4% since December (barring February). By contrast, ex-shelter services inflation remained soft, rising by just 0.04% on the month again, in turn reflecting softer price increases in medical care (-0.25%), transport and personal care.

In broad terms, today’s release can be seen as continuing to add to evidence that inflation is broadly in line with achieving the Fed’s target, consistent in our minds with a gradual removal of policy restriction over the coming quarters. However, the Fed’s – and broader market’s – focus has now shifted towards the labour market and a softer July report has reignited fears in markets of a sharper slowdown in activity ahead. In part, this should continue to reduce the emphasis on the monthly inflation reports as the Fed’s confidence of retaining anchored inflation expectations grows and its focus naturally shifts towards the outlook for inflation, not the outcome. That said, today’s report downplays some concerns that the Fed has overtightened policy – inflation looks likely to be coming down to around target rather than exhibiting signs of materially undershooting it. As such, we continue to view market expectations for 100bps of easing this year and another 100bp by this time next year as over-cooked. We expect the Fed to begin to gradual ease restrictive policy in September and forecast another cut in December. Beyond that outlook, we consider the outcome of November’s election as pivotal and beyond the honeymoon resurgence in Democrat fortunes under Vice President Kamala Harris’s candidacy, we still on balance expect to see Donald Trump return to the White House, something that we think could restrict the Fed’s ability to continue rate cuts in to next year.

Financial markets saw some reaction to a basically ‘in line’ outcome. Chances of a 50bps cut in September were scaled back by around 8ppt, now seen at a little over a one-third chance, but the market still almost fully prices 100bps of cuts by year-end. As such, 2-year US Treasury yields rose 4bps to 3.97% and 10-year 3bps to 3.86%. The dollar rose around 0.2% immediately after the release, but retraced all of those gains.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)

__________________________________________________________________________

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.