US reaction: September’s payrolls – Houston, we don’t have a problem

- 04 October 2024 (3 min read)

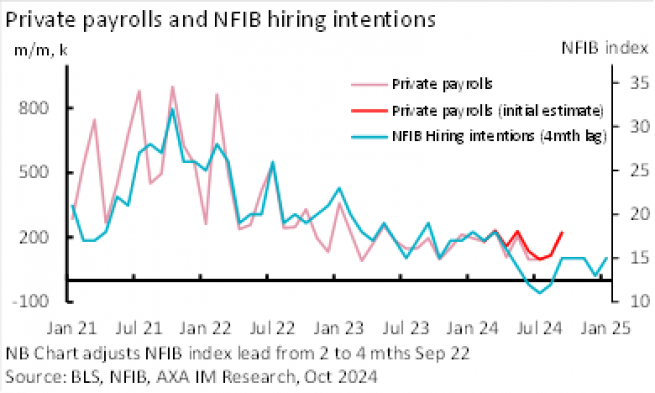

All eyes were on September’s payrolls after the unusually abrupt start to the Fed’s easing cycle, which had appeared spooked by signs of labour market softening. September’s report could not have been more “comforting” in that sense. Headline payrolls posted a surprise 254k gain – in excess of the above 150k consensus, and our own firmer estimate of 165k. Private payrolls rose by 223k, nearly 100k above consensus. Moreover, the prior 2 months were revised higher by 72k, August’s to 159k from 142k and July’s was revised back up to 144k from 89k. September’s 254k monthly gain is the strongest in six months and the 3-month trend (186k), still slower than in recent years, remains solid and its firmest since May. While there is some discrepancy with the level, Exhibit 1 illustrates that this improvement is in line with the pick-up in employment from the July lows signalled by the NFIB hiring index.

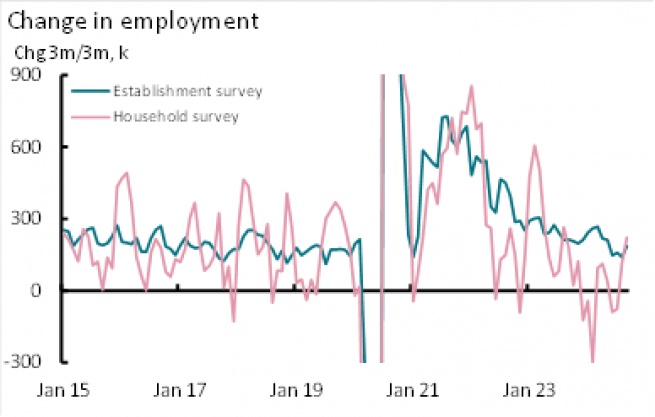

The household series posted even stronger gains, rising by 430k on the month and taking its 3-month average to 222k. The household survey is inherently more volatile than the payrolls series and in recent quarters we have been voicing some doubts about distortions (to the downside) through not fully capturing increased, migrant-driven labour supply. Nevertheless, as Exhibit 2 illustrates, in recent months even this series is pointing to firmer employment. This strong rise in employment led to a drop in unemployment to 4.1% (4.05% unrounded) from 4.2% (4.22%) last month. We are a little surprised at that and still suggest that post-employment volatility, with the prospect of slightly faster labour supply growth, should see unemployment end the year at 4.3%. But for now unemployment it is at its lowest since May. Moreover the Sahm metric is currently back below its 0.5% trigger threshold, having only exceeded it at 0.54% for one month last month.

Finally, average earnings posted their second successive month rising by 0.4% with the 3-month annualized pace of earnings now accelerating again to 4.3%, its highest since January’s spike and before that August 2023. The pace of earnings growth has only recently picked up with the annualized pace within a range that we would deem consistent with the Fed’s long-term inflation target from April to July. We also note that non-supervisory wage growth has not reflected this pick-up with 3-month annualized growth in this category at 3.5%. However, the total earnings figure is consistent with the lower unemployment rate and faster pace of employment growth recorded across the rest of the report.

The report will be an uneasy read for a Fed that appeared to deliver its abrupt 50bp easing last month on the back of weaker labour reports over the summer, that we had suggested would prove temporary. Today’s report will build some confidence of a more solid labour market ahead of what could be an incredibly noisy month in October. As things stand, next month’s print could be distorted by the dock workers and Boeing strikes, accounting for around 75k, plus any impact from the hurricane. At face value, next month’s labour market report could paint a more worrisome picture of activity, however, in the light of today’s strength the Fed should feel more confident about looking through the noise of that report. Moreover, we note that the NFIB survey, which continues to prove a good guide to underlying labour market activity, remained unchanged in its signal for next month, suggesting a solid ex-noise pace, and has risen in the latest month to suggest no deterioration in the labour market going into next year.

Indeed, we remain surprised by the Fed’s knee-jerk, 50bp cut in September and despite subsequent reassurances from Fed Chair Powell that this was not intended as a signal about the ongoing pace of cuts, we had sympathy for markets retaining some optionality that another ‘soft’ release could see the Fed react with another 50bps. Today’s report removes some of that risk. Indeed, we have argued that with the Fed implicitly endorsing the market’s aggressive path of easing over the coming 12-months, financial conditions no longer appear restrictive to us. Insofar as the Fed had suggested that it would keep policy restrictive enough to insure inflation reached the 2% target and remained there, the fact that is no longer the case raises the risks that inflation could start to drift higher again over the coming quarters.

This fact was not lost on markets. The short-term rate profile has now seen markets price only an 85% chance of a 0.25% cut in November, from near 30% chance of a 0.50% cut before the release. And for end-year, markets do not now fully discount two 0.25% cuts by year-end from expectations of nearly 50% of 75bps before the release. Further out, 2yr Treasury yields rose by 16bp to 3.89% and 10yr rose by 10bps to 3.95% (with 5y/5y breakeven edging higher to 2.30% - its highest since the start of August). The dollar also rose by 0.6% against a basket of currencies taking it to its highest levels since pre-Jackson Hole.

Related articles

View all articles

US reaction: Inflation slowing in line, but nothing weaker

- by

- 14 August 2024 (3 min read)

UK reaction: Confirmation for the Bank of England

- by

- 14 August 2024 (5 min read)

UK reaction: A further step in the right direction for the MPC

- by

- 13 August 2024 (3 min read)

US reaction: FOMC unch, but signals September

- by

- 01 August 2024 (3 min read)

UK reaction: Cautious cut, one more likely this year

- by

- 01 August 2024 (3 min read)

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.