US reaction: Services inflation makes pivotal shift lower

- 11 July 2024 (5 min read)

US CPI inflation surprised to the downside in June. Headline inflation dipped by 0.1% on the month compared to an expectation for a 0.1% rise, seeing the annual rate drop to 3.0% from 3.3% (3.1% expected) - the joint lowest rate since March 2021 (along with last June). The core rate, excluding fuel and energy, also came in softer than expected, rising by just 0.1% on the month compared to expectations for 0.2%. The annual rate slowed to 3.3% (from 3.4%) also the lowest reading for over three years.

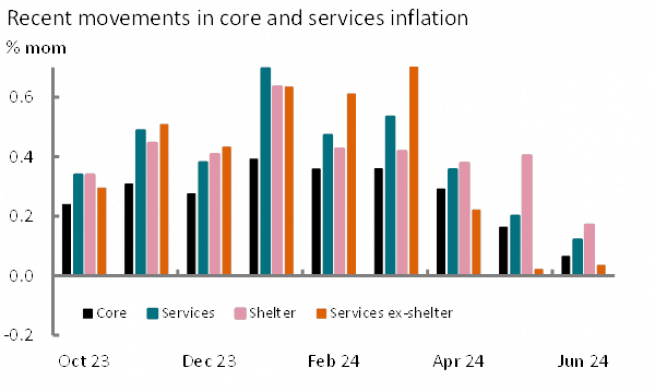

The fall in headline inflation was once again helped by a sharp fall in gasoline prices, motor fuel as a whole down 3.7% on the month. This helped broader commodities inflation to post its fourth consecutive monthly fall with only one month in the last 12 showing prices increases. Annual commodity price inflation is currently -0.4%. However, the Federal Reserve (Fed) has been focused on services inflation, which has been more persistently sticky and is more directly impacted by domestically generated inflation pressures, rather than the unwind of exogenous pressure including supply chain concerns. Annual services inflation has eased back in recent months and stood at 5.0% in June. While still elevated in annual terms, this understates the softening in recent months, with June’s monthly rise up just 0.12% - the smallest since January 2021 – following 0.36% in April and 0.20% in May. The composition of June’s services inflation also looks pivotal (Exhibit 1). While services ex-shelter posted another small rise in June, up just 0.04% after May’s 0.02%, shelter inflation appears to have finally cracked. This recorded a rise of just 0.17% having averaged a pace of 0.45% over the past 14 months. We have been expecting to see the drop recorded in new rents elsewhere feed through to the existing rents component of shelter inflation, but considered this only likely in H2 2024 as the six-month sampling of this series took effect. This looks like it has now emerged and we expect the coming months’ shelter inflation to be similarly subdued.

Fed Chair Powell reiterated at this week’s semi-annual monetary testimonies to Congress that the Fed required more evidence to gain sufficient confidence of softening inflation to ease monetary policy. However, at the June Fed meeting he had described May’s inflation data as “good”. June’s is better. With the Fed Chair also describing the labour market as “balanced” and displaying signs of “cooling” the Fed appears to be presented with inflation data that are becoming more benign and a softening in the labour market. We suggest that given the economic evidence, market pricing of <5% chance of a July cut appears stingy. In practice, with Powell remaining cautious just day’s earlier the Fed has laid the groundwork for a hold in July and there is little out between now and the Fed’s meeting on 31 July to scare them into an earlier move (the first estimate of Q2 GDP will be consequential, but expected at around 2% we do not expect it to precipitate a hurried reaction). As such we are comfortable with our view that the Fed will begin to ease policy only in September and still consider two hikes this year, penciling in a further cut in December.

Markets reacted predictably to today’s softer than expected inflation. The probability for a September cut rose from around 70% to just below 90%. Markets now price the chances of more than two cuts this (only around 15%) for the first time since early April (from only seeing an under 90% chance of two cuts). Longer-term yields followed the move, 2-year US Treasury yields down 14bps to 4.49% and 10-year yields and 10-year yields down 10bps to 4.18% - its lowest level since March. The dollar also softened dropping by 0.6% against a basket of currencies on the release.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.