Using short duration as a liquidity tool

- 27 May 2024 (5 min read)

For investors with large cash balances following the recent period of high interest rates, it may be time to start considering how the liquid allocation within their portfolio is positioned with rate cuts on the horizon. There is a case for considering short duration bonds for those investors looking to enhance performance of their liquidity portfolios while mitigating risk.

Short-dated bonds – A compelling alternative to enhance cash returns

Short-dated bonds typically have maturities up to five years, making them a potentially suitable bridge between cash holdings and longer-term fixed income investments. While riskier than cash, the higher returns on offer, limited volatility and natural liquidity of short-dated bonds should make them an attractive consideration for the liquid part of an investor’s portfolio.

There are key characteristics of short-dated bonds that make them particularly suited for liquidity management.

- Low volatility: Short-dated bonds tend to exhibit much lower price volatility compared to their longer-term counterparts, making them an attractive option for cash liquidity strategies.

- Natural liquidity pipeline: As short-dated bonds mature, the principal is returned to the investor, creating a natural liquidity pipeline. This reduces the need to trade and incur additional costs, further benefiting portfolio performance.

- Pull to Par: In environments where bonds are trading at a discount, the pull to par opportunity – where bonds are redeemed at their face value upon maturity – is attractive. This can potentially enhance returns, even when central bank rates are rising.

Reasons for short duration

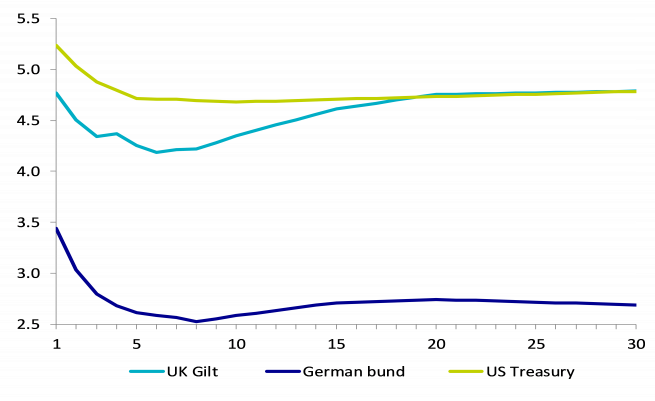

The inversion of sovereign yield curves, flat credit curves and continuing attractive yield valuations mean we continue to see opportunities in short duration strategies. As shown in the chart below, by investing in short duration strategies you should be able to minimise your duration risk while maximising your yield.

Short-dated bonds have proven their resilience over this hiking cycle, providing much better returns when compared to longer duration strategies. As we’ve now reached the peak of this hiking cycle, central banks may start cutting interest rates which should lead to falling cash rates. As such, there is an opportunity cost to remaining heavily invested in cash as short-dated bonds should outperform it by benefitting from the fall in sovereign yields on the back of lower interest rates.

Moreover, opting for active management offers additional advantages such as default risk mitigation, avoiding forced sales, and the potential for yield enhancement through careful bond selection. By considering short-dated bonds as part of a cash liquidity strategy rather than a traditional bond allocation, it may help investors optimise their portfolios and navigate the complexities of the current financial landscape.

Related Articles

View all articles

Fixed Income Market Update - June 2024

- by

- 26 June 2024 (3 min read)

Euro credit market update - June 2024

- by

- 25 June 2024 (3 min read)

Euro Long-Term Credit

- by ,

- 09 May 2024 (5 min read)

Emerging Market Debt: hope springs eternal

- by

- 12 April 2024 (5 min read)

Opportunities for High Yield Investors

- by

- 10 April 2024 (3 min read)

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.