Why now could be the time for ETF investors to consider the untapped potential of emerging markets credit

- 23 September 2024 (5 min read)

Although the ETF market is still dominated by passive equity, exciting product innovation in recent years means ETF investors now have more opportunity to build diversified portfolios across regions, asset classes, themes and styles.

One area which remains almost entirely untapped in ETFs, though, is emerging markets (‘EM’) corporate bonds. Several challenges in recent years – including the China property meltdown, tight US monetary policy, and global geopolitical tensions - have seen investors largely shun emerging market debt (‘EMD’). However, performance so far this year reminds us of some of the most compelling reasons to invest in the asset class: strong repricing opportunities and diversification benefits.

Year-to-date, investors have seen some remarkable returns from emerging market corporate bonds compared to other asset classes. The outperformance was mainly delivered by the strong credit return - the treasury return was fairly even, but the credit return for CEMBI BD (J.P. Morgan Corporate EMBI Broad Diversified Composite Index) was higher than for other asset classes.

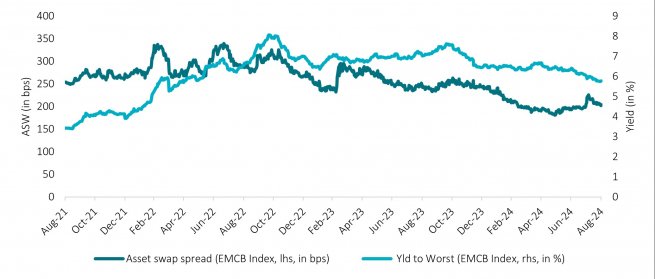

Since the start of the year, the ICE® BofA® Emerging Markets Corporate Plus Index has delivered 6.33% (as of 30 August 2024)*. Emerging markets received a further boost in late August, following US Federal Reserve (‘Fed’) Chair Jerome Powell’s speech at the Jackson Hole symposium (in which he indicated September’s forthcoming rate cut) and by the end of the month, EM corporate spreads stood at 202 basis points (‘bps’) with yield-to-worst at 5.76%. Even though spread levels are tight compared to historical levels, there are opportunities given the relative spread pickup to US credit. EM corporate bonds provide attractive yield while offering significant sector and country diversification across credit ratings.

Despite this strong performance, in our view, investors have far from missed out on potential gains in EM credit as there are good reasons to believe there’s more to come from the EMD recovery. In particular, the Fed have finally entered their easing cycle which should give more room for EM policy makers to cut their own rates. Indeed, we have already seen this from the Bank Indonesia, who kick started their own easing cycle with a 25 bps cut earlier in September.

We expect most emerging markets to stay the course on the fiscal side and disinflation, allowing for the positive chain effects from lower rates, higher growth, and improved debt dynamics to set in.

Overall, we see the current macro environment as a potentially beneficial backdrop for EM. Meanwhile, on the corporate side, EM corporates have increased their liquidity, the default cycle is largely behind us, and earnings growth has been healthy and revised higher on disinflation. In fact, gross leverage for EM corporates remains below that of US corporates. We expect rate cuts to help companies with financing cuts and that all of this could translate into attractive returns in EM credit for the remainder of this year and into the next. In our view, this is a compelling reason for ETF investors to explore opportunities to invest in EM credit.

Related articles

View all articles

Inflation Quarterly Update - January 2024

- by

- 23 January 2024 (3 min read)

Fixed Income Quarterly Update - January 2024

- by

- 23 January 2024 (3 min read)

US Investment Grade Market Outlook 2024

- by

- 09 January 2024 (5 min read)

US High Yield Market Outlook 2024

- by

- 09 January 2024 (5 min read)

How to consider a B/BB US high yield strategy within a portfolio

- by , ,

- 05 December 2023 (7 min read)

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.