Diversify portfolio risk with active fixed income ETFs

KEY POINTS

Every investor knows the cornerstone of building a portfolio is finding the right balance of risk and return potential to achieve certain investment objectives. All investment involves risk but usually the higher the potential return on offer, the higher the inherent risk involved as investors demand to be compensated for taking on more risk. The key is choosing the most suitable mix of asset classes such as equities (shares), fixed income (bonds), and perhaps alternatives such as property or commodities, according to the investment goals and risk tolerance of the investor.

Typically, equities and bonds behave quite differently in various market conditions, so, a combination of both can be considered a foundational risk management tool under the concept of diversification. Although it is widely acknowledged that a well-balanced portfolio should comprise a variety of equities and bonds, until relatively recently, many portfolios achieved equity exposure through passively managed ETFs and fixed income exposure through actively managed mutual funds. Active management is sometimes considered the more appropriate strategy for the complexity of the fixed income universe, but historically, there was little choice of active fixed income exposures within the ETF world. That is changing fast with exciting product innovations bringing a compelling choice active fixed income ETFs to the market.

The key risks for fixed income investors

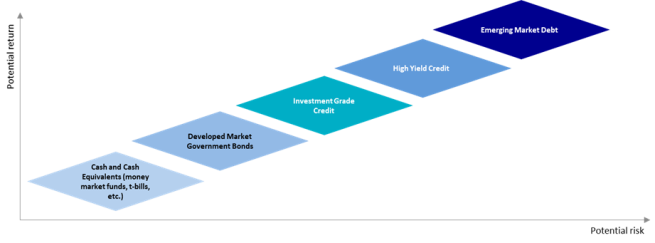

Bond returns should, generally speaking, be lower than equity returns through the economic cycle. They are a less risky asset class, as they are senior in the capital structure. Companies in trouble will always prioritise paying their bondholders, ahead of their shareholders. Therefore, a more ‘cautious’ portfolio will have a higher allocation to fixed income versus equities, while a more ‘adventurous’ portfolio will favour equities, with a smaller allocation to fixed income.

This does not mean that bonds are risk-free. Fixed income is a broad universe where investments come in a variety of guises. Among other factors, bonds vary in terms of lifespan, yields on offer, and of course, risk profile. The general rule of thumb dictates that government-issued bonds sit at the lower end of the risk spectrum while so-called high yield bonds inhabit the riskier end.

Broadly, where a fixed income sub-asset class sits on the risk spectrum depends on its expected exposure to two key factors: credit risk and interest rate risk. Understanding these risks is crucial for managing the overall profile of the portfolio.

As bonds are essentially ‘IOUs’ issued by corporations and governments looking to raise money, the main risk associated with fixed income investing is that the borrower may get into financial trouble and subsequently be unable to meet interest payments (coupons), or the issuer goes bust and is unable to repay the debt (principal) at maturity. Credit ratings assigned by independent bond rating agencies are used to assess the ability of the bond issuer to meet their obligations i.e. the potential level of credit risk. Developed market government bonds are seen as most reliable. But their perceived ‘safer’ status means they also offer very conservative yields. High yield bonds typically come with greater risk and are generally more volatile with higher default risk among underlying issuers versus investment grade bonds. But high yield issuers need to pay higher interest to incentivise potential investors.

Interest rate risk describes the inverse relationship of bond prices to interest rates. So as rates go up, as they did in 2022 and 2023, bond prices go down as new bonds coming to the market will offer higher coupons, and returns can be negative. Bonds with longer maturities and higher duration, are usually considered riskier versus shorter-dated counterparts, as long-term interest rate movements are less predictable, so their prices are more sensitive to changes in interest rates. However, it is not as simple as longer duration equals higher risk. For example, a shorter-dated bond issued by an emerging market government may still be considered riskier than a longer-dated bond issued by the US government.

How active management can help to mitigate fixed income risk

Weighing up the different risk factors can be complicated. For example, while high yield bonds are considered to have higher credit risk than investment grade bonds, they tend to have less interest rate risk due to typically being shorter maturity. Furthermore, the level of potential risk in any exposure can vary as markets move and economic conditions change.

This is where active management can help in terms of both navigating the complexity of the fixed income landscape by paying attention to these various risks in carefully selecting individual bonds for the portfolio, and in terms of flexibly adjusting exposures in response to market movements.

Active management of fixed income portfolios allows for a more efficient allocation of exposure to interest rate risk, credit risk, as well as individual sectors and countries. Passive allocations imply that investors need to have the same exposure indicated by a reference bond index, and typically, the bigger the weight of a bond, or a bond issuer in an index, the more indebted and therefore riskier it is. Active managers can aim to reduce exposure to the riskiest issuers and sectors.

On the credit side, they can use their expertise to identify and invest in high quality bonds, even in higher risk segments such as high yield global and euro credit markets. These approaches leverage thorough credit analysis, allowing for better assessment of issuer fundamentals and proactive adjustments to credit exposure to manage risk associated with credit quality, which is essential in a volatile market.

Another concept to bear in mind is that volatility does not equal risk. Volatility describes how much an asset’s price will move over the period it is held in the portfolio. Risk describes the likelihood of permanent capital loss – which occurs when the asset must be sold for less than it was bought. Volatility can be helpful, in that offers a window in which to buy assets at temporarily lower prices in hopes of a recovery. Embracing volatility is a key advantage of active management; it can be an opportunity for active managers to dynamically express their investment views. This adaptability can be crucial in capitalising on market dislocations and identifying mispriced assets.

Finally, there seems to be a common misconception that active ETFs are less liquid than their passive counterparts. However, it is essential to understand that liquidity primarily depends on the underlying securities and the ETF's investment strategy, rather than the active or passive nature of the fund itself. The ability to adjust holdings based on real-time liquidity assessments allows active ETFs to effectively navigate less liquid markets and select bonds with higher liquidity. Active fixed income ETFs continuously assess liquidity by examining trading volumes and market participant activity, while maintain portfolio diversification to reduce concentration risk and enhance liquidity, allowing for smoother responses to market shocks.

Building Blocks: Active Fixed Income ETFs

The global fixed income market is about $141 trillion in size, with over three million unique securities compared to only about 9,000 securities across global equity markets1. Passive ETFs can be a useful means of gaining broad fixed income exposure with high liquidity, but an active approach is best placed to access the full breadth and depth of the opportunity set.

In recent years, ETF investors have been increasingly demanding more choice in how to build well-balanced portfolios through their vehicle of choice. Active fixed income ETFs are an exciting innovation which combine ETF features such as ease of access, cost efficiency, and liquidity, with the benefits of actively managing fixed income risks and alpha opportunities, especially in terms of navigating the current uncertain market environment.

As such, there’s every reason to believe their growth in popularity will continue. In 2024, Active Fixed Income ETFs gathered $3.7bn – a huge increase from $230mn in 2023, while with another $1.9bn of flows so far this year (to 24 March), 2025 could be shaping up to be another record year for Active Fixed Income ETFs2.

AXA IM offers a range of active fixed income ETFs designed as asset allocation building blocks to gain exposure to large parts of the fixed income spectrum – from investment grade credit to high yield, across the US, Europe, and globally – providing flexible access to specific markets including some segments that may not be accessible in a passive ETF. The range also includes PAB (Paris Aligned Benchmark) ETFs which seek to align with a carbon transition strategy. The ETFs leverage AXA IM’s wide capabilities and expertise in active management, including over 25 years’ experience investing in fixed income markets. They can be utilised in the same manner as traditional mutual funds, serving as portfolio components or as a straightforward means of diversification.

- Source: AXA IM, Bloomberg as at 31/12/2024

- Source: AXA IM, etfbook as at 31/12/2024, 31/12/2023

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)