AXA WF Euro Credit Total Return achieves double figures

- 28 February 2025 (3 min read)

Key Points

Although launched in the Chinese calendar year of the Sheep, AXA WF Euro Credit Total Return has never been a fund that follows the herd. In 2015, markets were experiencing extensive central bank interventions that led to a strong compression of yield. It was, therefore, harder for investors to achieve attractive returns from fixed income using traditional, benchmark-aligned funds. Clients told us that they wanted an innovative and flexible strategy, able to adapt to periods of market volatility. They specified that it should aim to generate performance that was uncorrelated with both rates and credit markets.

With that in mind, AXA WF Euro Credit Total Return was developed to offer a flexible approach that, thanks to not having to follow a benchmark, could offer a strategic portfolio allocation with the aim of achieving risk-adjusted returns in different market conditions.

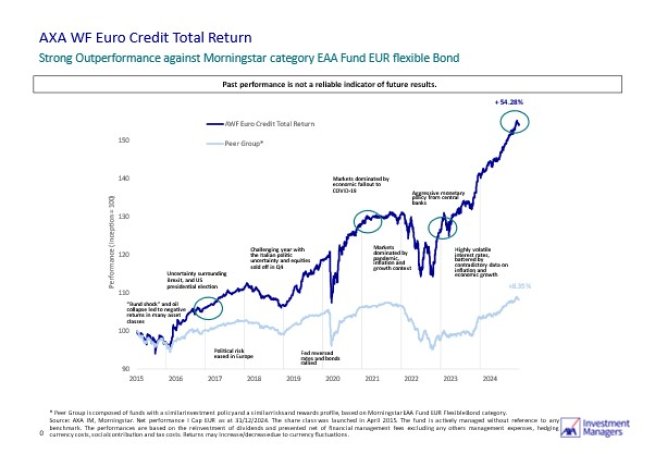

A journey of growth

Since its inception the Fund has posted an annualised total return of +5.26% (gross of fees) with volatility of 6.54%1 . Our mission as active portfolio managers is to deliver positive alpha by conducting rigorous research that supports astute sector allocation, security selection, and high conviction positions. As the chart below demonstrates, this process has been particularly important at times of high uncertainty such as Brexit, the economic fallout of COVID-19, and the central banks’ aggressive monetary policies that began in 2022.

Past Performance is not a reliable guide to current or future performance

- U291cmNlOiBBWEEgSU0gYXMgb2YgMzFzdCBKYW51YXJ5IDIwMjUgYmFzZWQgb24gRVVSIEkgc2hhcmUgY2xhc3MuIA==

The support investors have given the Fund is also a reflection of its successful track record. The Fund has seen substantial momentum as investors appreciate the potential benefits a flexible approach can have that incorporates a wide range of bonds across different sectors and capital structures. The AUM is now over €3bn having stood around €439mat the start of 20232 .

Behind the Fund is a euro credit team who have extensive experience investing across different market cycles and work collaboratively to share insights and best ideas. Through this team approach, the Fund’s philosophy and process has also evolved as it matured. One of those areas of growth is the strong ESG philosophy that the team embraced. They took the decision to transition the Fund into an ESG-integrated fund framework so it could be in line with Art.8 SFDR regulation3 . This ensures that the companies the Fund invests in are those identified as least likely to be impacted by material ESG risks at company or sector level.

- U291cmNlOiBBWEEgSU0gYXMgb2YgMzEgSmFudWFyeSAyMDI1

- VGhlIGNsYXNzaWZpY2F0aW9uIG9mIHRoZSBBWEEgV0YgRXVybyBDcmVkaXQgVG90YWwgUmV0dXJuIHVuZGVyIFNGRFIgbWF5IGJlIHN1YmplY3QgdG8gYWRqdXN0bWVudHMgYW5kIGFtZW5kbWVudHMsIHNpbmNlIFNGRFIgaGFzIGNvbWUgaW50byBmb3JjZSByZWNlbnRseSBvbmx5IGFuZCBjZXJ0YWluIGFzcGVjdHMgb2YgU0ZEUiBtYXkgYmUgc3ViamVjdCB0byBuZXcgYW5kL29yIGRpZmZlcmVudCBpbnRlcnByZXRhdGlvbnMgdGhhbiB0aG9zZSBleGlzdGluZyBhdCB0aGUgZGF0ZSBvZiB0aGlzIFByb3NwZWN0dXMuIEFzIHBhcnQgb2YgdGhlIG9uZ29pbmcgYXNzZXNzbWVudCBhbmQgY3VycmVudCBwcm9jZXNzIG9mIGNsYXNzaWZ5aW5nIGl0cyBmaW5hbmNpYWwgcHJvZHVjdHMgdW5kZXIgU0ZEUiwgQVhBIElNIHJlc2VydmVzIHRoZSByaWdodCwgaW4gYWNjb3JkYW5jZSB3aXRoIGFuZCB3aXRoaW4gdGhlIGxpbWl0cyBvZiBhcHBsaWNhYmxlIHJlZ3VsYXRpb25zIGFuZCBvZiB0aGUgQVhBIFdGIEV1cm8gQ3JlZGl0IFRvdGFsIFJldHVybuKAmXMgbGVnYWwgZG9jdW1lbnRhdGlvbiwgdG8gYW1lbmQgdGhlIGNsYXNzaWZpY2F0aW9uIG9mIHRoZSBGdW5kIGZyb20gdGltZSB0byB0aW1lIHRvIHJlZmxlY3QgY2hhbmdlcyBpbiBtYXJrZXQgcHJhY3RpY2UsIGl0cyBvd24gaW50ZXJwcmV0YXRpb25zLCBTRkRSLXJlbGF0ZWQgbGF3cyBvciByZWd1bGF0aW9ucyBvciBjdXJyZW50bHktYXBwbGljYWJsZSBkZWxlZ2F0ZWQgcmVndWxhdGlvbnMsIGNvbW11bmljYXRpb25zIGZyb20gbmF0aW9uYWwgb3IgRXVyb3BlYW4gYXV0aG9yaXRpZXMgb3IgY291cnQgZGVjaXNpb25zIGNsYXJpZnlpbmcgU0ZEUiBpbnRlcnByZXRhdGlvbnMuIEludmVzdG9ycyBhcmUgcmVtaW5kZWQgdGhhdCB0aGV5IHNob3VsZCBub3QgYmFzZSB0aGVpciBpbnZlc3RtZW50IGRlY2lzaW9ucyBvbiB0aGUgaW5mb3JtYXRpb24gcHJlc2VudGVkIHVuZGVyIFNGRFIgb25seS4=

Looking ahead

The outlook for fixed income markets remains nuanced: in Europe, stabilising inflation should enable the European Central Bank (ECB) to continue cutting rates into more accommodative territory. Things are more uncertain in the US, as President Trump’s aggressive policy stance poses a risk to inflation, potentially disrupting the Federal Reserves’s rate cut path. In the very short term, therefore, market may remain concerned about higher inflation and stronger growth in the US. While this is not a concerning scenario for credit, this may have an impact on the yield curve and hence on credit demand. From a spread perspective, we expect corporate credit risk premiums to move sideways in the coming months, implying that the key source of return will probably be carry.

On fundamentals, they should remain fairly supportive. Indeed, despite anemic growth in the Euro zone, we expect European companies’ credit metrics to stabilise or even improve. Financial discipline and cash preservation tend to remain a focus in Europe. As such, we don’t expect a wave of fallen angels or a jump in the default rate, although we expect the volume of rising stars to decline slightly during 2025.

Market technicals are hard to predict however they could also continue to be supportive; the reach for yield will probably continue and with lower ‘risk-free’ rates in 2025, we see no reason for the investment grade flows to stop. While on the supply side, after two years of massive primary issuance, we expect some stabilisation or even a potential deceleration in 2025.

Why the Fund is potentially attractive in today’s market

From a historical perspective, the euro credit asset class continues to offer significant yield over the last decade. The absolute yield available in the euro-denominated investment grade credit market sits at 3.27% above the 10-year historical average of 1.63%4 . As the ECB continues its easing cycle, we anticipate lower short-term rates and steeper yield curves. Our flexible duration management allows us to have exposure across the curve. In the past few years this has seen us prefer the short end of the curve. Now, with the expectation of lower short-term rates, we see potential to secure appealing income levels in longer-maturity credit.

Besides, the elevated levels of gross issuance in euro-denominated investment grade credit markets are creating opportunities for issuer selectors to capitalise on new issue premiums and unique investment stories. On a spread basis, we see euro denominated investment grade credit offering better relative value than other credit markets. Notably, the option-adjusted spread of the euro investment grade market currently exceeds the spread offered by US investment grade credit.

Overall, we believe that the euro investment grade market is supported by robust fundamentals. This combined with the growth divergence across eurozone countries and the current boom in issuance should bring investment opportunities for active portfolio managers. We therefore believe that AXA WF Euro Credit Total Return’s total return and flexible approach should offer investors an interesting solution that aims to adapt to any market environment.

Past Performance is not a reliable guide to current or future performance.

- U291cmNlOiBBWEEgSU0sQmxvb21iZXJnIGFzIG9mIDMxc3QgRGVjZW1iZXIgMjAyNA==

Calendar year performance5

The Fund is actively managed without reference to any benchmark.

*AXA WF Euro Credit Total Return launched on 25/02/2015.

- U291cmNlOiBBWEEgSU0gYXMgYXQgMzEgRGVjZW1iZXIgMjAyNC4gVGhlIGZ1bmQgaXMgQVhBIFdGIEV1cm8gQ3JlZGl0IFRvdGFsIFJldHVybiwgSSBFVVIgU2hhcmUgY2xhc3MuIFBlcmZvcm1hbmNlIHJldHVybnMgbWlnaHQgYmUgYWZmZWN0ZWQgYnkgY3VycmVuY3kgZmx1Y3R1YXRpb25zLiBOb3QgYWxsIHNoYXJlIGNsYXNzZXMgYXJlIGF2YWlsYWJsZSBpbiBldmVyeSBqdXJpc2RpY3Rpb24uIEludmVzdG9ycyBzaG91bGQgY2hlY2sgYXZhaWxhYmlsaXR5IHdpdGggdGhlaXIgQWR2aXNlci4gVGhlIGZ1bmQgaGFzIG5vIGluZGV4IHVzZWQgYXMgYSBwZXJmb3JtYW5jZSBpbmRpY2F0b3Iu

Key risks: AXA WF Euro Credit Total Return

The list below of risk factors is not exhaustive. Please refer to the prospectus for full product details and complete information on the risks.

Risk of capital loss: Except where the Prospectus explicitly references the existence of a capital guarantee at a given date, and subject to the terms thereof, no guarantee is made or supplied to investors with respect to the restitution of their initial or subsequent investments in a Sub-Fund. Loss of capital may be due to direct exposure, counterparty exposure or indirect exposure (e.g. exposure to underlying assets through the use of derivative instruments, securities lending and borrowing or repurchase agreement).

Counterparty risk: Risk of bankruptcy, insolvency, or payment or delivery failure of any of the Sub-Fund's counterparties, leading to a payment.

Liquidity risk: Risk of low liquidity level in certain market conditions that might lead the sub-fund to face difficulties valuing, purchasing or selling all/part of its assets and resulting in potential impact.

Credit risk: Risk that issuers of debt securities held in the Sub-Fund may default on their obligations or have their credit rating downgraded, resulting in a decrease in the Net Asset Value.

Impact of any techniques such as derivatives: Certain management strategies involve specific risks, such as liquidity risk, credit risk, counterparty risk, legal risk, valuation risk, operational risk and risks related to the underlying assets.

Risk related to investments in high yield instruments: The Fund may be exposed to a risk related to investments in high yield financial instruments. These instruments present higher default risks than those of the investment grade category. In case of default, the value of these instruments may decrease significantly, which would affect the Net Asset Value of the Fund

The use of such strategies may also involve leverage, which may increase the effect of market movements on the Sub-Fund and may result in significant risk of losses.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (AXA IM) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA IM in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA IM excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA IM is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA IM is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA IM does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd.