CIO Views: Investors bullish on US equities despite high valuations

KEY POINTS

Chris Iggo, CIO AXA IM Core

US equities: Price vs. value

The US equity market’s valuation is a recurring investor concern. On some estimates, the S&P 500 is priced at 22 times estimated 12-month forward earnings. On the same measure, the Nasdaq 100 is priced at 26 times. These are high valuations. The equity earnings yield is the inverse of the price-to-earnings ratio - a lower yield represents a potentially overvalued index - and for the S&P 500, it is currently 4.54%, just above the 10-year US Treasury yield (4.23%). Even the equally weighted S&P 500 multiple is priced at 19.8 times expected earnings. When we calculate price-earnings ratios on an inflation and cyclically adjusted basis, the S&P 500 is at the 90th percentile of its 1995-2024 history. A broader measure puts the US at its 93rd percentile valuation ranking since 1983. No other major equity market comes anywhere close to the US’s current valuation level.

But valuation is no guarantee of future returns. Investors seem bullish on US equities with earnings growth expected to be 14% over the next year and President-elect Donald Trump’s policy agenda appears supportive. But a valuation adjustment is a risk if fundamentals or sentiment quickly deteriorates. Other assets are cheaper than US stocks – including Europe and Asia equities and, importantly, US Treasuries. Like other government bonds, Treasuries have cheapened on a relative value basis to swaps and corporate bonds. A rapid rotation out of stocks into bonds could be one of the great surprises of 2025.

Alessandro Tentori, CIO Europe

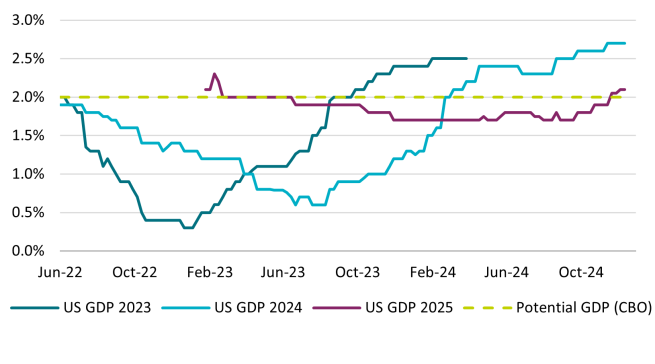

No ‘surprise effect’ in 2025

During the past 24 months, we’ve witnessed a significant repricing of US GDP estimates. Initial estimates for 2023 were in the range of 0.3% - 0.5%, while growth turned out to be a solid 2.5%. Similarly, the consensus expected 2024’s US GDP to grow around 1.3% at the end of 2023, while realised growth is probably closer to 2.7% (see chart). The market’s reaction followed suit with an equally impressive acceleration in the S&P 500’s earnings-per-share growth, thus beating pre-season expectations in seven of out of the last eight quarters. Our impression is the consensus might have improved substantially both in terms of macroeconomics as well as for markets for 2025. US GDP forecasts are starting from a higher base compared to both 2023 and 2024, as the consensus expects the economy to grow by 2.1% (AXA IM forecasts 2.3%). According to Bloomberg, median expectations for the S&P 500 are at 6,600 points at the end of 2025 - quite a shift in mood from a rather downbeat initial expectation for the end of 2024 at 4,800 points. Therefore, we might have to live without the strong ‘surprise effect’ seen in the past two years, despite a faster than potential GDP growth. This does not necessarily mean the stock market’s performance will be disappointing in 2025, but rather that the bar for yet another result in excess of 20% is unmistakably high.

Ecaterina Bigos, CIO Asia ex-Japan

Multispeed in a multipolar world

Diverging macroeconomic and geopolitical dynamics are expected to drive complexity for Asia’s economies in 2025, and this will require astute management of fiscal and monetary policy.

Confidence in India’s growth has deteriorated, given the slowdown in industrial activity, urban consumption and private investment. With increased need for fiscal consolidation, some monetary easing may be warranted. Inflation, however, is above target and subject to large weather-related shocks in food prices. Arguably as one of the most domestically oriented economies in Asia, with a relatively closed capital account and a limited trade footprint, India is less susceptible to direct trade tensions.

Korean externalities were an increasing risk leading up to December’s political events. Growth is challenged by the cyclical weakness in global manufacturing, downside risks to automobile exports, and the uncertain outcome of the likely US tariffs. Internally, consumer demand is weak, notwithstanding the impact from a likely drop in inbound travel. Fiscal policy has room to boost demand, while monetary policy is restricted by elevated household debt.

Taiwan is showing economic resilience, with year-on-year momentum more backloaded. Growth has benefited from semiconductor and servers demand and order visibility.

High performance computing demand and investment are expected to stay, as artificial intelligence supply chains are building capacity. Non-technology exports face headwinds and the trade surplus with the US is likely to get scrutinised. When it comes to policy, residential property market leverage limits potential easing.

Asset Class Summary Views

Views expressed reflect CIO team expectations on asset class returns and risks. Traffic lights indicate expected return over a three-to-six-month period relative to long-term observed trends.

| Positive | Neutral | Negative |

|---|

CIO team opinions draw on AXA IM Macro Research and AXA IM investment team views and are not intended as asset allocation advice.

Rates | Divergence between US and European rates outlook | |

|---|---|---|

US Treasuries | Modest further Fed easing expected but yields in fair value range | |

Euro – Core Govt. | Significant ECB rate cuts priced in | |

Euro – Peripherals | Fiscal and political concerns could underpin volatility in early 2025 | |

UK Gilts | Signs of slower growth should bring yields down | |

JGBs | Yields to head modestly higher | |

Inflation | Upside risks to US inflation should become priced in |

Credit | Investor confidence in credit market remains strong | |

|---|---|---|

USD Investment Grade | All-in yields remain attractive and demand is strong | |

Euro Investment Grade | ECB rate cuts to support returns from investment grade credit | |

GBP Investment Grade | Attractive yields but concerns over macro outlook | |

USD High Yield | Stronger growth, resilient fundamentals, and higher quality universe are supportive | |

Euro High Yield | Resilient fundamentals, technical factors and ECB cuts support total returns | |

EM Hard Currency | Healthy growth backdrop and attractive yields to support performance |

Equities | Donald Trump’s policy agenda seen as supportive for US equities | |

|---|---|---|

US | Q3 earnings growth looks to be robust with financials and technology leading | |

Europe | Weak growth could impact earnings growth expectations | |

UK | Clarity on fiscal and regulatory plans required for UK equities to do better | |

Japan | Resilient global growth is supportive; reforms, monetary policy key for sustained performance | |

China | Data remains weak and market awaits more stimulus in 2025 | |

Investment Themes* | Secular spending on technology and automation should support relative outperformance |

*AXA Investment Managers has identified six themes, supported by megatrends, that companies are tapping into which we believe are best placed to navigate the evolving global economy: Technology & Automation, Connected Consumer, Ageing & Lifestyle, Social Prosperity, Energy Transition, Biodiversity.

Disclaimer

The information on this website is intended for investors domiciled in Switzerland.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not liable for unauthorised use of the website.

This website is for advertising and informational purpose only. The published information and expression of opinions are provided for personal use only. The information, data, figures, opinions, statements, analyses, forecasts, simulations, concepts and other data provided by AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) in this document are based on our knowledge and experience at the time of preparation and are subject to change without notice.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) excludes any warranty (explicit or implicit) for the accuracy, completeness and up-to-dateness of the published information and expressions of opinion. In particular, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not obliged to remove information that is no longer up to date or to expressly mark it a such. To the extent that the data contained in this document originates from third parties, AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) is not responsible for the accuracy, completeness, up-to-dateness and appropriateness of such data, even if only such data is used that is deemed to be reliable.

The information on the website of AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group) does not constitute a decision aid for economic, legal, tax or other advisory questions, nor may investment or other decisions be made solely on the basis of this information. Before any investment decision is made, detailed advice should be obtained that is geared to the client's situation.

Past performance or returns are neither a guarantee nor an indicator of the future performance or investment returns. The value and return on an investment is not guaranteed. It can rise and fall and investors may even incur a total loss.

AXA Investment Managers Switzerland Ltd (Part of BNP Paribas Group)